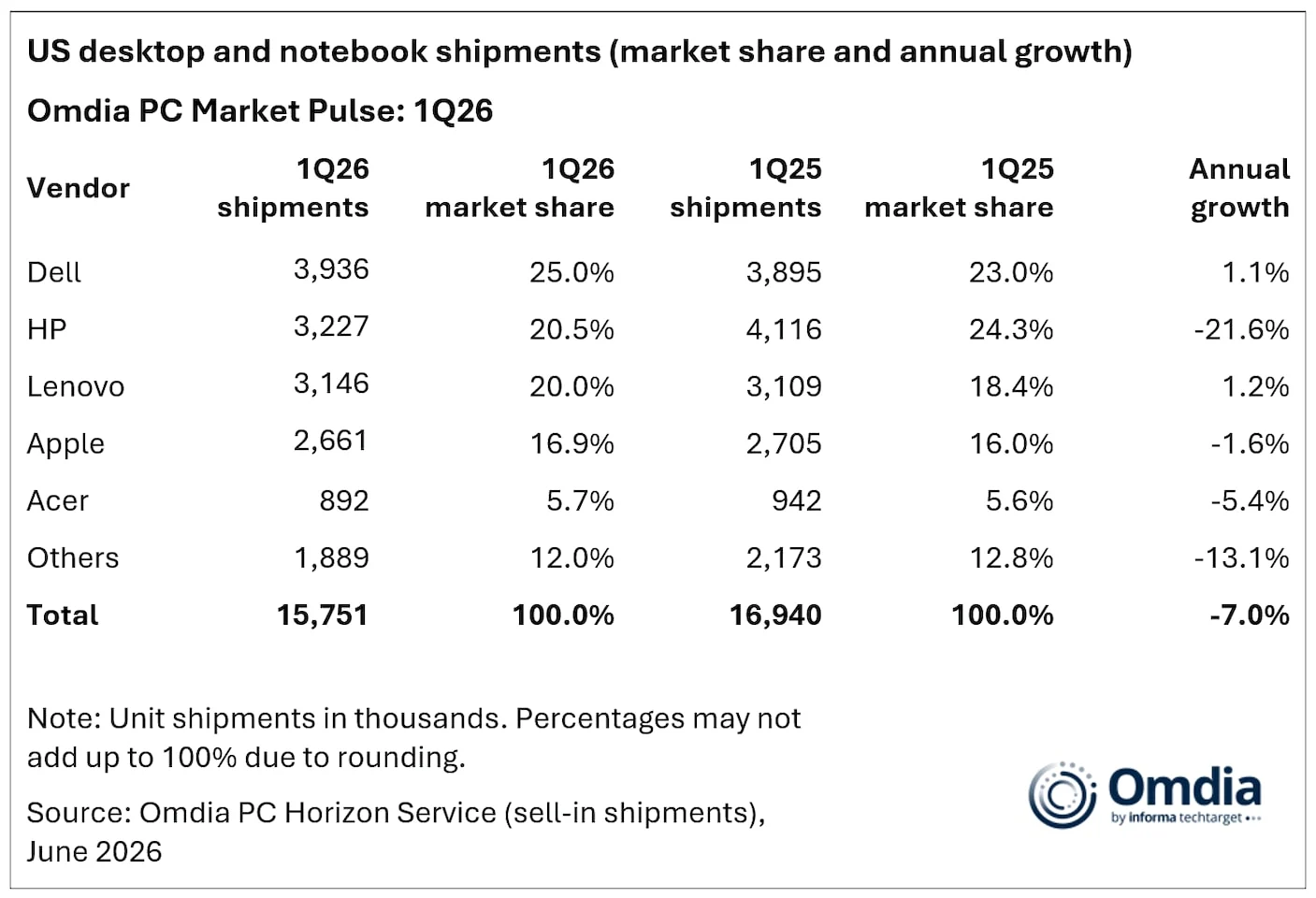

The US personal computer market witnessed a significant downturn in the first quarter of 2026, with shipments dropping by 7.0% to 15.8 million units. This decline, the most severe since late 2023, is largely attributed to component supply constraints, surging memory and storage costs, and a cooling of demand following the recent Windows 11 upgrade cycle.

Key takeaways

- Total US PC shipments fell 7.0% year-over-year in Q1 2026.

- Component shortages, particularly for DRAM and NAND, are driving up prices and limiting low-end device availability.

- AI-capable PCs now account for 44% of all shipments, contributing to rising average selling prices.

- Business demand remains more resilient than the consumer segment despite overall market contraction.

Impact of component constraints and shifting demand

Supply chain issues have been exacerbated by the diversion of key components toward high-demand artificial intelligence server applications. This has disproportionately impacted entry-level PCs priced under $500, a segment that saw an 18.7% decline. While business hardware updates continue to provide a crucial floor for the market, consumer demand has sagged as buyers grapple with higher price tags and unfavorable economic conditions.

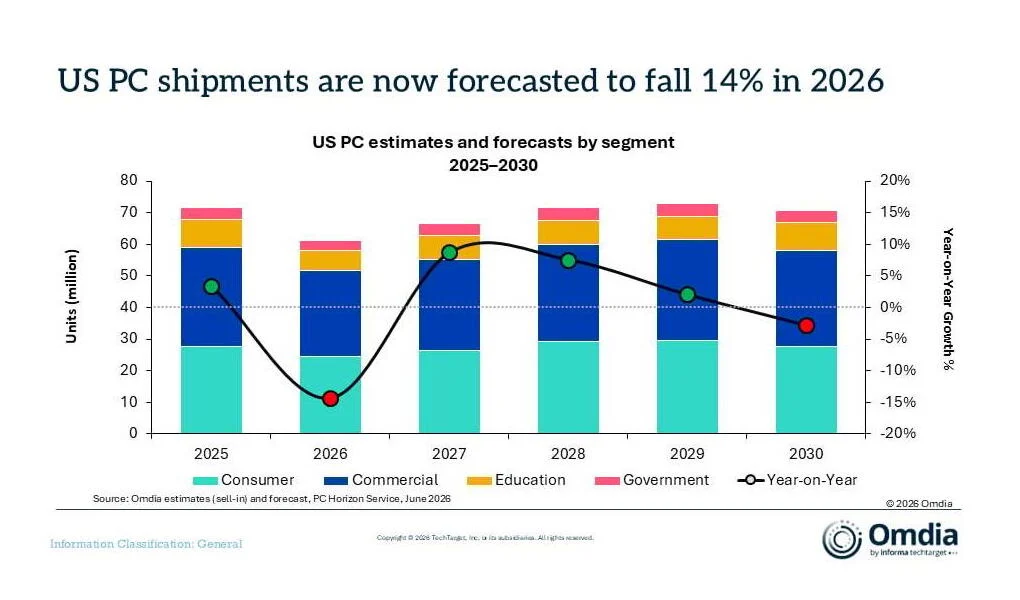

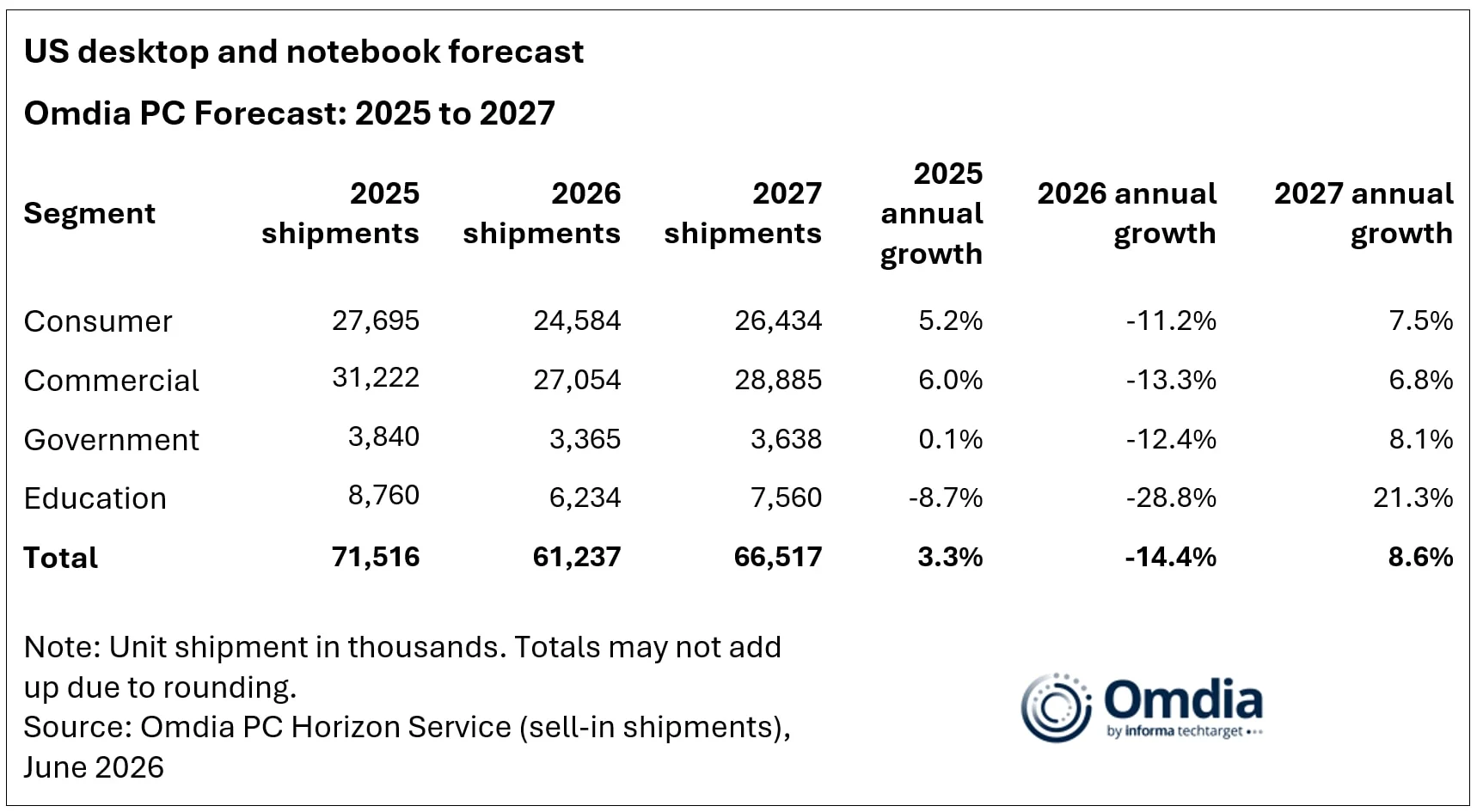

Forecasts suggest that total shipment volume for 2026 will likely decline by 14.4% compared to 2025. Rising costs are expected to keep entry-level prices elevated through at least 2027, temporarily suppressing broader consumer interest.

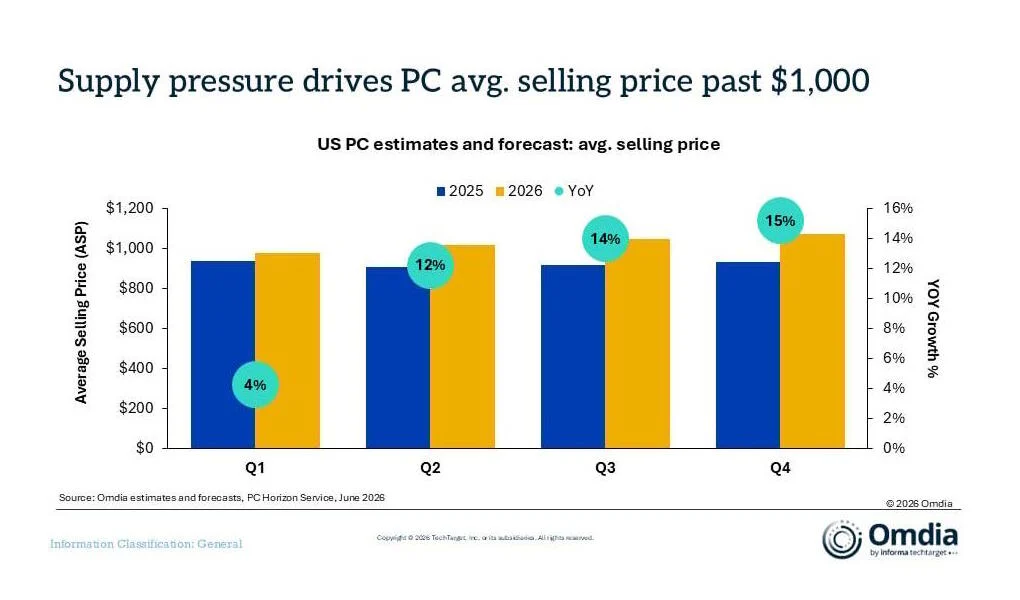

Rising prices and AI adoption

Average selling prices for PCs are climbing, fueled by both supply-side constraints and a major market shift toward artificial intelligence. Nearly 44% of all machines shipped in the first quarter were “AI-capable,” with large enterprises showing a strong preference for these premium offerings. Analysts expect average selling price growth to accelerate to over 12% in the second half of 2026.

Vendor performance shifts

Market dynamics varied significantly among major manufacturers during the quarter, leading to a shake-up in top-tier rankings. Dell emerged as the market leader with a 25% share, posting slight growth of 1.1%. Lenovo also saw modest success, reaching a 20% market share. Conversely, HP experienced a sharp 21.6% decline, causing it to lose its previous top position. Apple outperformed the broader market, maintaining nearly 17% of the total share as its presence in the business sector continues to expand. In contrast, smaller vendors struggled to maintain their footing, facing a 13.1% decline as they lacked the procurement leverage enjoyed by the industry’s largest players.

Via Omdia