A significant spike in demand for NAND Flash storage, driven by booming AI server deployments and supply shortages, led the top five global suppliers to post a remarkable revenue surge in the first quarter of 2026. These market shifts are reshaping priorities in data storage and technology infrastructure worldwide.

Key Takeaways

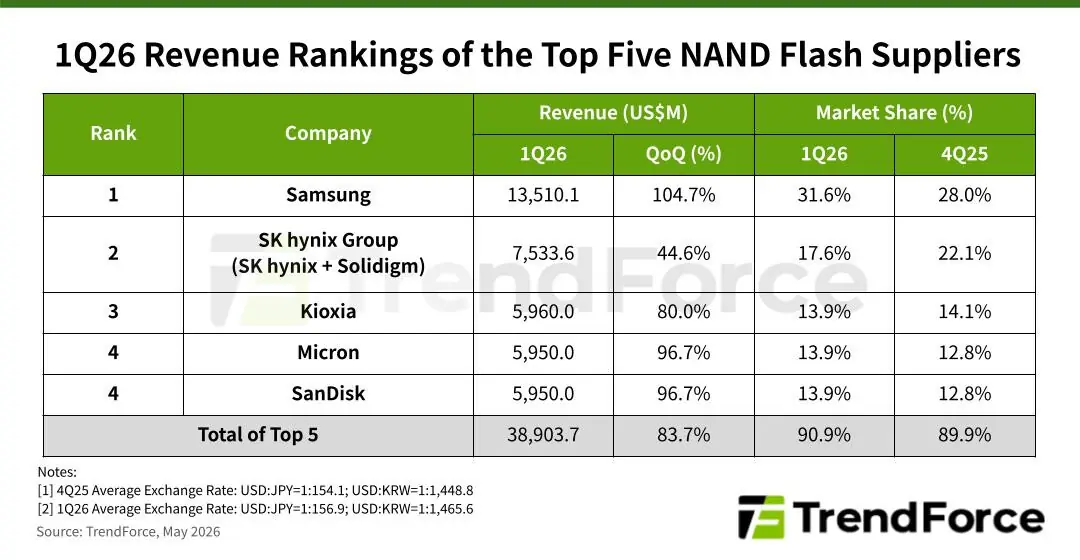

- Combined revenue of the top five NAND Flash suppliers rose 83.7% quarter-over-quarter, reaching over $38.9 billion.

- Persistent supply shortages gave rise to substantial price increases and changed the competitive landscape.

- Suppliers are focusing production on high-capacity enterprise SSDs amid elevated demand from AI server initiatives.

Surge Driven by Enterprise Needs and Market Imbalances

Demand for enterprise SSDs skyrocketed as cloud service providers and AI infrastructure projects raced to expand high-speed, large-scale data storage capabilities. This was further accelerated by a structural shortage of traditional hard drives, shifting more orders toward NAND-based solutions, especially QLC enterprise SSDs.

Amidst robust demand, the average selling price (ASP) for NAND Flash products soared, surpassing market forecasts. The resulting revenue for the sector outperformed expectations, setting new records for quarterly growth.

Top Suppliers: Market Leaders and Growth Rates

A closer analysis of individual supplier performance in 1Q26 reveals:

Samsung retained its top position by leveraging contract pricing advantages and substantial increases in server-focused shipments. Notably, Sandisk more than tripled its data center business quarterly, reflecting a shift to high-value product lines and aggressive market maneuvers.

Industry Trends and Outlook for 2026

Looking forward, industry analysts forecast that the unusual supply-demand gap for NAND Flash will persist through 2026. Despite higher prices impacting general PC and smartphone demand, server orders are projected to offset these declines.

Key trends shaping the market include:

- No significant capacity expansions are planned by major suppliers for the year, with existing output prioritized for enterprise applications.

- NAND Flash products featuring 200 or more layers are poised to become the mainstream standard by year-end.

- High-capacity QLC enterprise SSDs will continue to capture expanding market share.

As suppliers maintain their disciplined capacity utilization and pricing power, continued elevated revenue and profitability are expected throughout the year.

Conclusion

The NAND Flash industry’s extraordinary growth in the first quarter of 2026 underscores the centrality of advanced storage in AI-driven tech landscapes. As suppliers respond to the unrelenting pace of data center expansion, the competitive race to provide cutting-edge memory solutions is set to persist well into the foreseeable future.

Via TrendForce